In his previous White Paper on Financial Statements (click here in case you missed it), TobinLeff partner and former Ernst & Young CPA, Chuck Gottschalk, addressed topics like what data buyers will be looking for and what kind of information and documents you should provide when selling your company.

In this follow-up White Paper, Chuck digs deep into two very important issues:

- How important are accurate financials, and why are they critical to the price you will ultimately get for your firm?

- What are some common adjustments to financial reporting that can leave you with more money in your pocket after a sale?

Click here for theory and case studies on how to improve your own financial portrait: TL Preparing Financial Statements Part 2 White Paper

Preparing Your Financial Statements for a Sale of Your Company, Part II: Accuracy and Adjustments

In our most recent White Paper titled, “Preparing Your Financial Statements for a Sale of Your Company,” we discussed how important the way in which you present your financial information is to the value you ultimately will receive from the sale of your firm. In this White Paper, we cover two additional topics that, when coupled with the prior piece, will give you a complete architecture for optimizing your financial presentation.

The first topic covers the importance of accuracy in financial statements at both the summary level and within the underlying detailed records and how it can increase company value for a sale. The second addresses common adjustments that should be made when presenting numbers to potential buyers so that they can clearly understand the cash flow of the business.

How important are accurate financials?

As we said in the first White Paper: “Very.” But, you probably do not have audited financial statements. While you may use outside accountants, you are likely to have them prepare reviewed or compiled statements. Compilations and reviews do not include an accountant’s stated opinion that the financial statements are accurate in all material ways. It is rare for an independent firm to have audits prepared, because they are significantly more expensive.

So, how do you – and, equally importantly, a buyer – know that your statements are accurate? If you have a quality accountant/controller/CFO on your team, you likely trust the results that they present to you as you have gained confidence in that person over time. If you don’t have such a person, or even if you do, when a potential buyer’s CPA comes in to analyze your results, without an independent accountant’s audit opinion they have no basis to have the same confidence that the financials are accurate. This is why the buyer will insist on a comprehensive due diligence process, and why they will ask for and comb through your detailed records before actually closing a deal.

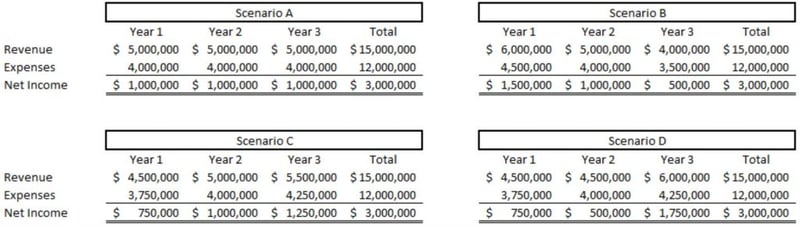

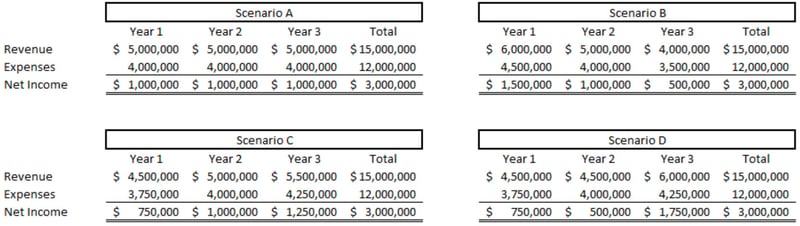

Interestingly, one of the things we have learned from the many deals we have facilitated at TobinLeff is that sellers’ financial statement inaccuracies often understate the value of their company to their own disadvantage. A common cause for this is recognizing revenue in the wrong period. For example, let’s assume that a company has $15 million of revenue over a three-year period and $3 million of net income (these figures are chosen for ease of math, but the principles apply equally to much larger and much smaller firms). Below are potential ways to get to those identical end results:

Each of these scenarios paints a very different picture. In Scenario A, we see a stable firm whose business is flat. Scenario B shows a company with declining revenue, margins, and profits. In Scenario C, the firm enjoys increasing revenue, margins, and profits, and Scenario D presents a (realistically) fluctuating business. All other things being equal, a buyer likely will pay the most (or offer the best terms) for a company with the results in Scenario C, and the least for Scenario B, with Scenarios A and D somewhere in the middle.

But what is often the case is that a company actually performing under Scenario C presents the results of Scenario D. So, one of the questions we ask when we are representing a TobinLeff client is: Does the historical financial scenario you are presenting represent the most favorable way to honestly show your results? We review your previous year’s financials and re-visit the decisions made to look for anomalies that may present themselves. The first metric is always one of accuracy; the second is whether honest revisions can be made to improve the picture. To simply accept previously reported results and not challenge them can be a mistake that will result in a lower valuation or a buyer asking for a reduction in purchase price. Frequently, these adjustments revolve around the timing of recognition of income and expenses, and, as we all know… Timing is everything!

In the event that the review of previous periods indicates that a shifting of revenue or earnings is required to accurately and optimally reflect the results of operations, it will be necessary for you to thoroughly document the reasons for these changes with a written explanation prepared in advance. When the buyer’s outside accountants review your financial statements as part of due diligence, they will likely uncover documents that you cannot change that reflect the previously reported results. For example, tax returns are a common way for a buyer’s accountants to verify the results presented. By having this written explanation available, it will validate the revised reporting. In fact, we will generally present this written explanation on behalf of our clients when we provide their detailed data to buyers in order to create an environment of full transparency.

Anyone who has been involved with a number of mergers and acquisitions transactions is familiar with what can best be described as “deal fatigue.” This is what happens at the end of the deal – and often just before closing – when the buyer comes back to the seller and states, based on the CPA’s analysis of the financial statements, that they need to reduce the price they will pay. This creates a highly emotional moment in which excited sellers suddenly find themselves doubting that the big check they saw in their future is ever going to materialize. Most often calmer heads prevail and the deal gets done, but this deal fatigue and the highly charged negative emotional moment may be avoided by making certain that financials are accurate from the start.

Finally, you need to consider the accuracy of interim financial results. A buyer will almost always ask for year to date operating results during the acquisition process. If the acquisition begins in January, not much credence will be given to one month’s results. But if the sale occurs later in the year, it is possible that a buyer will place more weight on the interim results than the previous year’s results and, as such, the accuracy of these interim numbers must be evaluated. Once again, timing rears its massive head.

For example, it is not uncommon for one company to record an entire year’s bonus to be paid to employees at the end of the calendar year and another company when it is paid in the following year. This type of policy can have many unintended consequences that result in inaccurate financials. If the entire year’s bonus is not recorded as an expense until December, then the interim financial results likely overstate the income. Alternatively, if the bonus is recorded as an expense when paid in January and the interim financials are through June, then the six-month results will, in effect, have twelve months’ worth of bonus expense, thereby understating net profits.

Other common examples of items that can create a distortion of interim results are 401(k) matches and corporate liability insurance expenses which are paid and expensed in one month’s results while actually reflecting a full year’s activity. A quick review of 12 individual months of year-over-year operating results shown side by side should draw these items out to ensure accurate interim statements.

Common Adjustments in Presenting Financial Results During a Sale

When evaluating a potential business acquisition, buyers want to understand not just the historical performance as presented in the financial statements, but also what normalizing adjustments are necessary to reflect the true economic results of operations that the buyer will experience upon purchase. Equally importantly, as the seller’s representative, at TobinLeff we want to make sure that all appropriate adjustments are made to present our client’s results in the most favorable and value-driven light. Following is a list of some of the more common normalizing adjustments that we always explore:

Executive Compensation and Related Party Compensation – Often, owners pay themselves a salary that is not consistent with what a non-owner in that role would command as a fair market rate. In some cases, the owners pay themselves below market rates as a way to minimize contributions to social security tax, and in other cases they pay above market rates and include some or all of their profit distribution in salary, bonus, or guaranteed payments. Some business owners also choose to employee family members as directors or in other roles in which compensation is not truly tied to performance. In all of these cases, adjustments need to be made that can either enhance or reduce financial results.

Related Party Rent – In the event that there is a related party lease for personal or real property, these leases should be evaluated to determine if they are in line with market rates. We have seen cases where this amount is either significantly above or below the market.

Discretionary and Personal Expenses – Although business owners are often reluctant to disclose personal expenses, it is in their best interest to come up with a comprehensive list. Common examples include the purchase or lease of automobiles, country club dues, contributions to charities, and premiums for life insurance policies that would be used to fund a buyout. In all of these cases, these expenses represent potential “add-backs” that will increase the bottom line and, accordingly, the value of your company.

Former Employee Compensation – Sometimes a company offers itself for sale a few years after a former owner has been bought out. These buy-outs sometimes contain clauses that the selling party will receive compensation and benefits on a go-forward basis while providing little or no ongoing support to the operations. These facts must be disclosed with appropriate adjustments made to both historical results and projections.

Extraordinary or Non-Recurring Income and Expense – Items that occurred but are not expected to occur in the future, such as legal settlements (paid or received), insurance proceeds, acquisition costs, and many others, offer more add-back opportunities. Note: The treatment of Paycheck Protection Program (PPP) forgiveness should not automatically be classified in this category. The amounts received from PPP need careful consideration and are outside the scope of this White Paper. Feel free to reach out to me at cgottschalk@tobinleff.com if you would like to discuss how PPP might impact your sale value.

Cash to Accrual – One of the most commonly overlooked adjustments in recasting earnings is the potential to present numbers on an accrual basis. Buyers tend to prefer to see accrual basis financial statements, yet many independent firms report on the cash basis due to ease in preparation and potential tax advantages. Fortunately, almost all of the most common accounting packages allow for either cash or accrual basis reporting, and getting a set of accrual financial statements may be as easy as the click of a button. If you are going to click that button, you will want to make sure that your accountants and advisors have the insights to convert your financial statements to a true accrual basis. Although that button will take you 90% or more of the way there, you will need to commit a few hours to assuring yourself that everything worked as intended.

As an example of the cash vs. accrual divide, look back at the four scenarios shown in the first section of this White Paper. The difference between Scenarios C and D could be the result of the use of the cash method of accounting in one case and accrual in the other. Another example discussed earlier is when the expense for bonuses is recorded.

The Bottom Line: Your Bottom Line

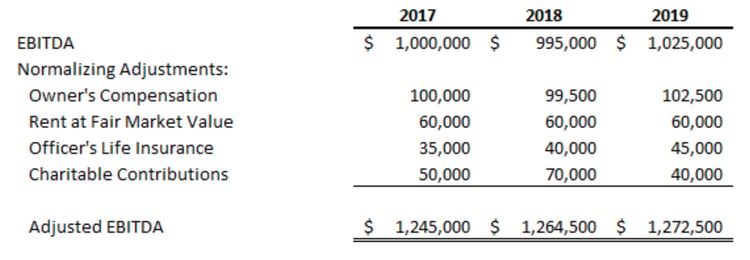

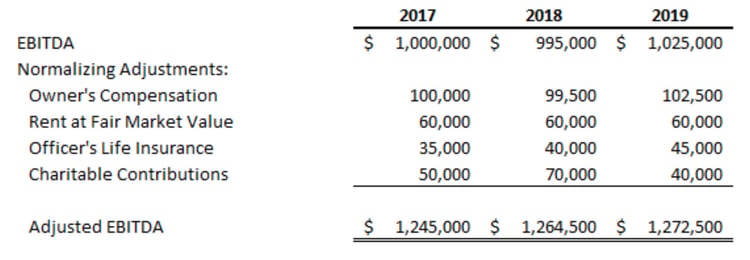

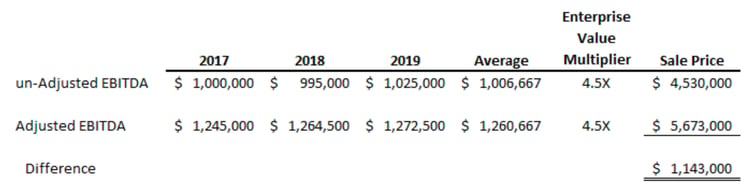

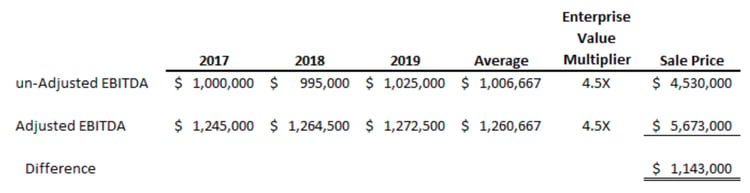

Why does all of this matter? Here is a sample case of normalizing adjustments:

Before these sample normalizing adjustments (yours, of course, will be specific to your own financials), the average EBITDA for these three years is $1,006,667; after normalizing adjustments, $1,260,667. Using the most common valuation formula of applying a multiple to Adjusted EBITDA, and demonstrating this with a middle of the road 4.5x multiplier for these numbers, we get a pre-adjustment firm value of $4,530,000, and a post-Adjustment value of $5,673,000.

So, the question for you to ask yourself is this: Is an extra $1,143,000 in the value of my business worth the effort to get my financials in shape and to hire an advisor who knows how to present them for me in the best possible light and has the contacts to approach the greatest number of potential buyers?

How important are accurate financial statements when selling your firm?

Very.