What's Inside

- An earnout is a provision in which a portion of your agency's purchase price is deferred and paid based on meeting future performance benchmarks — typically over 1 to 5 years post-close.

- Earnouts are common in agency transactions because buyers are purchasing future cash flow, not history. They shift some risk from buyer to seller while giving sellers upside if the business performs.

- Sellers generally prefer earnout metrics tied to top-line revenue (AGI); buyers generally prefer bottom-line metrics (EBITDA or Net Income). The negotiation between these two positions is where deals are shaped.

- Operating control during the earnout period is one of the most important — and most overlooked — provisions to negotiate. If your payout is tied to EBITDA, you need to control the variables that affect it.

- A well-structured earnout has a floor and a ceiling, clearly defined accounting methods, interim payments, key employee retention incentives, and a change-of-control clause.

- Based on TobinLeff's experience advising on over 250 agency engagements, the most common earnout period is three years, with a range of one to five.

If you own a marketing agency or professional services firm, you will almost certainly encounter earnout provisions when the time comes to sell. If you are a buyer with a buy and build growth strategy, you will likely be structuring them into your offers.

Either way, the terms of your earnout agreement will directly shape your net worth and your peace of mind for years after the deal closes. Whether you are preparing to sell, actively in the process, or evaluating an offer right now, this article breaks down 12 elements of earnout design and negotiation that every agency owner should understand.

What Is an Earnout in an Agency Sale?

An earnout agreement is an arrangement between a seller and a buyer in which a portion, or in some cases all, of the purchase price is contingent on the business's future performance after the transaction closes.

It is a mechanism that shifts some of the risk from the buyer to the seller, while granting the seller meaningful upside opportunities if the agency performs.

A portion of the selling price is deferred and calculated based on whether the business meets defined performance metrics over a set period.

Why Are Earnouts So Common in Agency M&A Transactions?

When you sell a marketing or professional services agency, what you are really selling is the future cash flow of the business. Your historical performance provides credibility and gets you to the table, but sophisticated buyers base their valuations primarily on what they believe the business will generate going forward.

Earnout provisions exist to give buyers assurance that clients will stay, key employees will remain, the agency is not dangerously dependent on the selling owner, and there is clear evidence of a sustained growth trajectory.

They also exist because most sellers believe their agency is worth more than a buyer's initial valuation reflects. Earnouts bridge that gap. They allow the business to prove its worth over time rather than forcing both sides to agree on a single fixed number at close.

From a mechanics standpoint, earnouts are financing instruments that use the business's future cash flows to supplement the upfront cash and debt a buyer brings to fund the transaction. They create aligned incentives: sellers stay engaged post-close, transitions run more smoothly, and buyers have a structural safeguard against overpaying.

12 Elements of a Well-Structured Earnout Agreement

Based on TobinLeff's experience crafting exit plans and advising on over 250 agency engagements — both sell-side and buy-side — here are the 12 elements we consider best practices when designing and negotiating earnout terms.

1. How Should Performance Metrics Be Structured?

The metrics used to track earnout performance should be selected so that both the seller and buyer win when benchmarks are achieved. In most agency transactions, sellers prefer that the scorecard be based on top-line performance — typically Adjusted Gross Income (total revenue minus media and outside services purchased) — because it has the most direct influence on revenue generation. Buyers typically prefer bottom-line metrics such as Net Income or EBITDA, which account for how efficiently the business is being run.

In some situations, deferred payments may be tied to non-financial metrics such as retaining specific clients or continued employment of key personnel.

Keep the performance metrics to one or two benchmarks wherever possible. Avoid all-or-nothing threshold structures. Instead, use linear or scaled earnings metrics that reward incremental performance and reduce the risk of a near-miss costing the seller a disproportionate amount.

2. How Are Interim Payments Handled During an Earnout?

Sellers understandably do not want to wait until the end of a three- to five-year period to receive all deferred compensation. Most earnout agreements are structured with cash at closing plus interim payments made annually or quarterly throughout the earnout period.

Interim payments may have performance strings attached to protect the buyer. At the conclusion of the earnout period, a final "true-up" payment is calculated as the total purchase price minus the cash paid at closing minus the sum of all interim payments already made.

3. Who Controls Operations During the Earnout Period?

If you are the seller, operating control during the earnout period is among the most critical provisions you will negotiate — and among the most frequently underestimated.

If your purchase price is tied to meeting Net Income or EBITDA benchmarks, you must retain meaningful control over the variables that directly affect those numbers. Define the seller's operational rights clearly in the Purchase Agreement or Operating/Shareholders' Agreement.

Get the buyer's written commitment to leave operations largely unchanged during the earnout period.

If the buyer insists on new investments or additional expenses beyond historical levels, negotiate that those specific costs be treated as add-backs to the Net Income or EBITDA calculation. This ensures you are not penalized for expenses you did not choose and cannot control.

4. How Should Cross-Selling Be Handled After the Sale?

If you sell to a strategic acquirer, a larger agency or holding company, cross-selling is frequently cited as one of the primary rationales for the transaction. Both sides want to leverage the other's client relationships, capabilities, and staff.

Without clear written terms, cross-selling can create significant conflict during the earnout period. Define the structure in advance. One approach is to establish internal transfer rates — typically 10–20% below standard client rates — for work sent between entities. This structure rewards the seller for cross-selling the buyer's clients while preserving the buyer's margin when full rates are billed externally.

Critically, if the buyer sends work to the seller, the seller should not be penalized in the earnout calculation for having their resources redirected. Internal rates provide the mechanism to compensate for that redirection.

5. What Should the Growth Plan Look Like?

Sophisticated buyers may pay strong multiples when they believe an acquired agency will contribute meaningfully to their broader financial targets. When that is the case, the buyer and seller should jointly develop a growth plan and define the investments required to execute it before the deal closes.

Once defined, both sides must agree in writing on how those investments will be treated in the earnout calculation. The goal is to avoid a situation in which the seller is incentivized to make short-term decisions that maximize their earnout at the expense of the business's long-term health.

In one recent TobinLeff transaction, we negotiated a provision in which the buyer's growth investments were treated as add-backs to the EBITDA calculation, ensuring the seller was not penalized for expenses the buyer had committed to incurring.

6. Should Earnouts Have a Floor and a Ceiling?

Sellers naturally prefer an uncapped earnout formula — the higher the agency performs, the higher the payout. Most experienced buyers, however, build in a ceiling to limit their maximum exposure. Best practice is to negotiate both a floor and a ceiling that are equitable to both parties.

For example, if the target purchase price is 5.0x EBITDA, the guaranteed floor might be 3.5x and the ceiling might be 6.5x based on performance. This structure gives the seller downside certainty while preserving meaningful upside for strong execution.

7. How Long Should an Earnout Period Last?

The most common earnout period in agency transactions is three years, with a range of one to five years. Buyers typically prefer longer periods — they reduce risk and spread out payments. Sellers generally prefer shorter periods to minimize the time their payout is at risk.

The tracking period can incorporate both historical and forward-looking windows. In one recent TobinLeff transaction, we structured a four-year EBITDA average using the trailing twelve months plus the forward thirty-six months. This approach gave the buyer confidence rooted in recent performance while still creating a meaningful forward-looking incentive for the seller.

8. How Should Key Employees Be Incentivized During the Earnout?

If the seller's upside is contingent on future performance, the agency's key employees should have aligned incentives; otherwise, the seller is carrying disproportionate risk.

Two common structures accomplish this.

- A Phantom Stock Plan allows select employees to earn a percentage of the seller's purchase price as it is paid out, provided they remain employed.

- A Stay Bonus Plan pays employees a defined bonus if they remain with the company for a specified period after close. Both structures are welcomed by buyers because they reduce the risk that key employee departures will derail the transition.

9. How Are Earnout Payments Taxed?

Tax treatment is one of the most financially significant and most frequently overlooked elements of earnout design. Sellers want as many deferred payments as possible to be taxed as capital gains. Buyers prefer some payments classified as ordinary income so they can realize immediate deductions.

When structured properly, the IRS, under general tax principles (Arrowsmith v. Commissioner, 344 U.S. 6), allows deferred payments to qualify for installment sale treatment and to be taxed as capital gains to the seller. It is critical to identify early in the negotiation whether deferred payments will represent: (i) deferred purchase price payments eligible for installment sale treatment, (ii) compensation for continued employment, or (iii) payments for a non-compete covenant. Each classification carries different tax implications for both parties.

Engage qualified M&A tax counsel before finalizing earnout terms. The difference in after-tax proceeds can be substantial.

10. What Happens to the Earnout If the Buyer Sells During the Earnout Period?

This is a protective clause that sellers should insist on, and buyers will typically resist. A change-of-control provision stipulates that if the buyer sells the business during the earnout period, all deferred payments immediately vest and become payable to the seller upon close of that transaction.

Without this clause, a seller can find themselves mid-earnout when their buyer is acquired — operating under new ownership with no guarantee that the conditions supporting their earnout will be preserved. This provision is a fundamental seller protection.

11. How Are Disputes Resolved During the Earnout Period?

Earnout provisions should clearly define the accounting method used to track performance and the process for resolving disputes. Most agreements specify GAAP accounting standards as the measurement framework.

For dispute resolution, the agreement should stipulate that an appointed third-party CPA or consulting firm serves as the arbitrator if the parties cannot reach an agreement. Ambiguous language about how revenue is recognized, how expenses are allocated, or how add-backs are calculated is one of the most common sources of post-close conflict. Define it precisely before you sign.

12. Why Does Clarity in Earnout Terms Matter More Than Anything Else?

Whether you are a buyer or a seller, clarity is the most valuable thing you can build into an earnout agreement. Ambiguity does not protect either party; it creates conflict, delays payments, and in some cases unravels transactions entirely.

Take the time before close to define, negotiate, and put in writing: the key performance metrics, the operating guidelines during the earnout period, the growth plan and how investments are treated, the governance structure, the dispute resolution process, and every material contingency you can anticipate.

A well-drafted earnout is not a concession — it is a structure that allows both sides to transact with confidence.

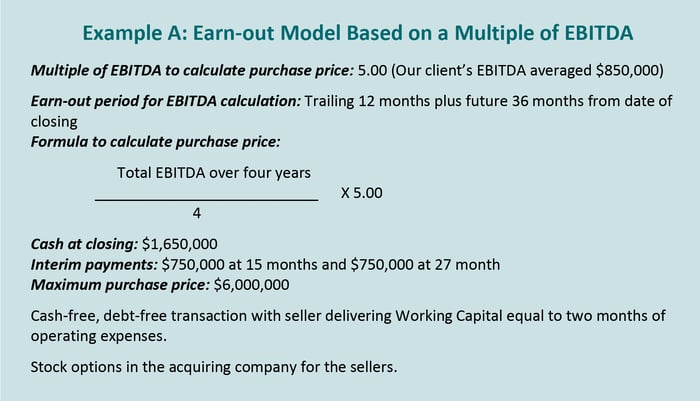

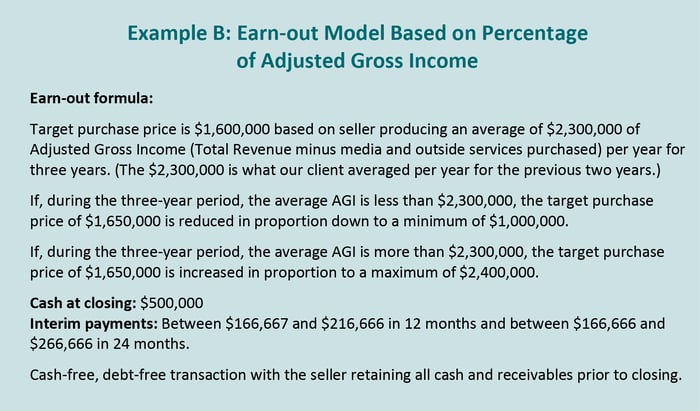

Sample Earnout Formulas

TobinLeff recently designed and negotiated two earnout formulas for sell-side clients that illustrate how structure follows context.

The first formula was based on a multiple of EBITDA. It was used because the seller was maintaining a separate profit center during the earnout period and the buyer required a profit-based metric. The seller retained meaningful operating control and negotiated that the buyer's growth investments would be treated as EBITDA add-backs.

The second formula was based on a percentage of Adjusted Gross Income. It was used because the seller's agency was being immediately integrated into the buyer's enterprise — meaning the seller would have limited control over the expense side of the P&L. An AGI-based metric reflected what the seller could actually influence post-close.

Both transactions incorporated the majority of the 12 elements described above to protect our clients' interests.

Warning Signs: Earnout Mistakes Agency Sellers Make Most Often

These are the patterns TobinLeff sees most frequently, and the ones that most reliably erode seller value or create post-close conflict:

-

Agreeing to metrics you can't control. If your earnout is tied to EBITDA but the buyer controls hiring, overhead, and investment decisions, you are at significant risk. Never agree to bottom-line metrics without negotiating operating control provisions.

-

Skipping the change-of-control clause. If the buyer sells mid-earnout and you haven't protected yourself, your deferred payments are in jeopardy.

-

Accepting all-or-nothing thresholds. Binary earnout structures, where missing a benchmark by a small margin costs the seller a disproportionate payout, are unnecessarily punitive. Push for linear or scaled formulas.

-

Ignoring tax structure until it's too late. The classification of deferred payments as capital gains vs. ordinary income is not a minor detail. Engage tax counsel before finalizing terms, not after.

-

Failing to align key employee incentives. If your top people have no financial reason to stay post-close, your ability to hit earnout benchmarks is compromised from day one.

-

Leaving cross-selling terms undefined. In strategic acquisitions, undefined cross-selling arrangements create resource conflicts and P&L disputes that can damage both the earnout and the relationship with the buyer.

-

Relying on a generalist attorney. Agency M&A transactions have nuances that general business counsel is not equipped to navigate. The earnout provisions in your Purchase Agreement require advisors who have seen these structures before.

Frequently Asked Questions: Earnouts When Selling a Marketing Agency

What is an earnout in an agency sale?

An earnout is a provision in an acquisition agreement where a portion of the purchase price is deferred and paid after closing, contingent on the acquired agency meeting defined performance benchmarks over a set period. Earnouts are common in agency transactions because they bridge the valuation gap between what sellers believe their firm is worth and what buyers are willing to pay upfront based on risk.

How common are earnouts in marketing agency transactions?

Earnouts are a standard feature of most marketing agency and professional services transactions, particularly for firms with founder-dependent revenue, meaningful client concentration, or limited track record at current margins. Based on TobinLeff's experience advising on over 250 agency engagements, a deferred payment structure is present in the majority of deals.

How long does a typical earnout last when selling an agency?

The most common earnout period is three years, with a range of one to five years. Buyers typically prefer longer periods to reduce risk; sellers typically prefer shorter periods to minimize how long their payout remains at risk. In some transactions, the measurement period incorporates both trailing historical performance and forward projections.

Should earnout metrics be based on revenue or EBITDA?

This is one of the central negotiations in any earnout structure. Sellers generally prefer revenue-based metrics (such as Adjusted Gross Income) because they reflect what the seller can most directly influence. Buyers generally prefer profit-based metrics (EBITDA or Net Income) because they reflect how efficiently the business is managed. The right answer depends on how integrated the agency will be post-close and how much operating control the seller will retain.

What is a floor and ceiling in an earnout agreement?

A floor is the minimum guaranteed purchase price — the amount the seller receives regardless of performance. A ceiling is the maximum the buyer will pay, regardless of how well the agency performs. A typical structure might set a floor at 3.5x EBITDA, a ceiling at 6.5x, and a target at 5.0x. Both the floor and ceiling should be explicitly negotiated and documented.

What is a change-of-control clause in an earnout?

A change-of-control provision stipulates that if the buyer is acquired or sells the business during the earnout period, all deferred payments immediately vest and become payable to the seller. This protects the seller from finding themselves mid-earnout under a new buyer who may not honor the original operating conditions. Buyers typically resist this clause; sellers should insist on it.

How are earnout payments taxed for agency sellers?

When structured properly, deferred earnout payments can qualify for installment sale treatment and be taxed as capital gains for the seller. However, payments classified as compensation for continued employment or non-compete covenants are taxed as ordinary income. The tax treatment of each payment component should be identified and structured before the deal is finalized. Engage qualified M&A tax counsel early in the process.

What is Adjusted Gross Income (AGI), and why does it matter in earnouts?

Adjusted Gross Income — sometimes called Net Revenue or Net Fees — is total revenue minus media costs and outside services purchased on behalf of clients. It represents the revenue the agency actually retains and is a more accurate reflection of the firm's economic output than gross billings. AGI is frequently used as an earnout metric in agency transactions where the seller has limited post-close control over expenses.

How do I protect my earnout if the buyer starts making decisions that hurt my margins?

Negotiate operating control provisions before the deal closes. The Purchase Agreement or Shareholders' Agreement should specify the buyer's commitment to leave operations materially unchanged during the earnout period. If the buyer plans to make investments or incur expenses above historic levels, those costs should be treated as add-backs to the EBITDA or Net Income calculation so the seller is not penalized.

What should I do to prepare my agency for a transaction that includes an earnout?

The most important steps are: understand which metrics will drive your earnout and begin managing to them before the sale process begins; address client concentration so your revenue is not disproportionately dependent on one or two clients; lock in key employees with retention incentives; and ensure your financial reporting is clean, accurate, and GAAP-compliant. Sellers who enter the process with organized financials and stable performance metrics command stronger terms and move through due diligence faster.

Glossary of Key Earnout Terms

-

Earnout: A contingent payment structure in which a portion of the purchase price is paid after closing, tied to the acquired company meeting specific financial benchmarks over a defined period.

-

Adjusted Gross Income (AGI): Total revenue minus media costs and outside services purchased on behalf of clients. The revenue figure the agency actually retains is commonly used as a top-line earnout metric.

-

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. A standard measure of operating profitability used in agency valuations and as a bottom-line earnout metric.

-

Net Income: Profit after all operating expenses, interest, and taxes. Sometimes used as an earnout metric when buyers want performance tracked at the fully-loaded profit level.

-

Floor: The minimum guaranteed purchase price the seller receives regardless of post-close performance.

-

Ceiling: The maximum purchase price the buyer will pay, regardless of how strongly the agency performs during the earnout period.

-

True-Up Payment: The final payment made at the conclusion of the earnout period, calculated as the total earned purchase price minus cash paid at closing minus all interim payments already made.

-

Change-of-Control Clause: A provision stipulating that all deferred earnout payments immediately vest and become payable if the buyer sells the business during the earnout period.

-

Phantom Stock Plan: A retention mechanism in which select employees earn a percentage of the seller's purchase price as it is paid out, provided they remain employed through the earnout period.

-

Stay Bonus: A cash bonus paid to key employees who remain with the company for a defined period post-close, used to reduce turnover risk during the earnout period.

-

Installment Sale Treatment: An IRS provision that allows deferred payments to be taxed as capital gains for the seller rather than as ordinary income, subject to proper structuring. Engage qualified M&A tax counsel early in the process.

-

Add-Back: An adjustment made to EBITDA or Net Income to account for expenses that are non-recurring, buyer-imposed, or otherwise not reflective of the seller's normalized operating performance.

-

Letter of Intent (LOI): A non-binding document outlining the key terms of a proposed acquisition — including purchase price, deal structure, and earnout framework — before a definitive agreement is negotiated. Well drafted LOIs may contain a mix of binding and non-binding provisions.

-

Purchase Agreement: The definitive legal document governing the sale, including all earnout provisions, operating control rights, performance metrics, and dispute resolution mechanisms.

About TobinLeff

Owners of leading marketing agencies, PR firms, digital agencies, and professional services businesses trust TobinLeff to sell their firms. We are an investment banking and M&A advisory firm guided by our values of always doing what's right and what needs to be done to produce results.

By combining an extensive network of strategic buyers and private equity partners with hands-on, end-to-end guidance and superior financial acumen, our clients realize outstanding outcomes — strong valuations with buyers whose values, culture, and vision align.

TobinLeff has advised owners through over 250 transactions. If you are thinking about selling your agency in the next two to five years, the best time to start a conversation is before you think you need to.

Schedule a confidential conversation today.

Click here for your complimentary copy: TL 12 Elements of Earn-outs White Paper